COMPANY NEWS

Essex Bio-Technology Reports Stellar 2024 Annual Results:Net Profit soars 11.6% to HK$ 307.2 Million, Dividend increases 33.3% Focuses on Strengthening R&D Capabilities and Expanding Market Access

2025.03.26

Download

Hong Kong, 26 March 2025

Results Highlights:

Results Highlights:

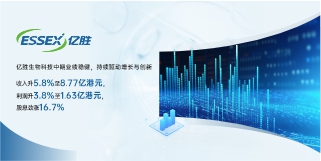

- Net profit climbs 11.6% to HK$ 307.2 million, with net profit margin improves to 18.4% from 15.8% in 2023, the result of operational efficiency.

- Final dividend proposed at HK$6.0 cents per share, bringing the total dividend for 2024 to HK$12.0 cents per share, a 33.3% increase compared to 2023.

- Obtained NMPA approval for the registration and commercialisation of Diquafosol Sodium Eye Drops and Sodium Hyaluronate Eye Drops (0.3%).

- Secured an exclusive agency right in the PRC for SCALGENTM double-layered artificial dermis.

- New BFS manufacturing line for Beifushu® unit-dose eye drops installed and near-completion of a new eye gel manufacturing line.

- A total of 100 patents certificates or authorisation letters, comprising 70 invention patents (發明專利), 15 utility model patents (實用新型專利) and 15 design patents (外觀專利).

- Covering more than 14,000 hospitals and medical providers, and with approximately1,810 pharmaceutical stores across the PRC.

- Honours in Recognition of the Group’s Innovation and Quality:

- 2024 Forbes Asia’s Best Under A Billion list

- China Excellent IR - The Best Capital Market Communication Award and The Best Digitalised Investor Relations Award

- Zhuhai Essex Bio-Pharmaceutical Company Limited was awarded as one of the 第六批國家級專精特新“小巨人”企業名單 (The 6th National-Level "Little Giant" Specialised and Innovative Enterprises List).

- Zhuhai Essex Bio-Pharmaceutical Company Limited was awarded as one of the 2023年度TOP100中國化藥企業 (2023 Top 100 Chemical Pharmaceutical Companies in the PRC)

- Beifushu® Eye Drops - 2024 Excellent Brand of Biochemical and Biological Pharmaceutical

- Beifushu® - Chinese reputable medicine brands (in six consecutive years)

Essex Bio-Technology Limited (“Essex” and its subsidiary the “Group”, Stock Code: 1061.HK), a leading biologic Group that develops, manufactures and commercialises genetically engineered therapeutic recombinant bovine basic fibroblast growth factor (“rb-bFGF”). Today, the Group announces its robust annual results for the year ended 31 December 2024.

Despite challenges in the pharmaceutical landscape, Essex Bio-Technology achieved remarkable profitability growth, expanded its market presence, and drove R&D innovation. In the PRC, the pharmaceutical industry faced significant headwinds in 2024, including centralised procurement policies that pressured drug prices and reshaped the competitive landscape.

However, Essex Bio-Technology demonstrated its resilience by adapting swiftly to the evolving market environment, enhancing cost control while ensuring quality assurance, and leveraging its strengths in innovation and operational efficiency. These strategic efforts enabled the Group to deliver steady financial performance and achieve sustainable growth in a challenging year.

Core Products Drive Revenue Growth

The Group delivered net profit growth of 11.6% year-on-year to HK$307.2 million, with the net profit margin improved to 18.4% from 15.8% in 2023. Total turnover for 2024 was approximately HK$1,669.8 million, a 3.9% decrease as compared to HK$1,737.0 million in 2023, primarily due to pricing pressure from the centralised procurement policies in the PRC (“Policy’s Impact”). Despite this, the Group upholds its market position through the broadening of indications for its flagship biologics and expansion of patient access.

The Beifushu® series and Beifuji® series, the Group’s flagship products, continued to be the primary growth drivers, contributing 84.5% of total turnover. The ophthalmology segment recorded a turnover of HK$771.5 million, up 2.2% year-on-year, supported by strong demand for eye care products. The surgical segment generated HK$879.9 million, a decrease of 9.3% due to the Policy’s Impact, but remains a key pillar of the business.

Ample Liquidity and Healthy Financial Position

The Group maintains a healthy financial position, as at 31 December 2024, the Group recorded cash and cash equivalents of approximately HK$557.2 million. Bank borrowings stood at HK$165.3 million, with a distributed repayment schedule: 42.2% repayable within 1 year, 25.5% in 1 to 2 years, and 32.3% in 2 to 5 years. The Group’s gearing ratio improved to 28.8% (2023: 32.0%), reflecting its prudent financial management and strong liquidity.

The Board is pleased to propose a final dividend of HK$6.0 cents per ordinary share. Together with the interim dividend of HK$6.0 cents per ordinary share, the total dividend for 2024 reaches HK$12.0 cents, representing a notable year-on-year increase of 33.3% from HK$9.0 cents in 2023, which demonstrated the Group continues its effort to deliver higher rewards to its shareholders.

Extensive Range of Products Driving Growth in Ophthalmology and Surgical Fields

The Group’s business is primarily made up of the ophthalmology segment (“Ophthalmology”), surgical (wound care and healing) segment (“Surgical”) and provision of services segment. Additionally, the Group is pursuing new therapeutics in oncology, orthopaedics and neurology through strategic investments.

Currently the Group has six commercialised biologics, collectively referred to as the “bFGF Series”, which are marketed and sold in the PRC. Three of the bFGF Series were approved by NMPA as Category I drugs, and four are listed on the National Drug List for Basic Medical Insurance, Work-Related Injury Insurance and Maternity Insurance in the PRC.

In addition to the bFGF Series, the Group has a portfolio of commercialised preservative-free unit-dose eye drops, including Tobramycin, Levofloxacin, Sodium Hyaluronate (0.1%, 0.3%), Diquafosol Sodium and Moxifloxacin Hydrochloride Eye Drops.

Strategic R&D Investment Driving Growth

The Group is committed to pragmatically investing in new products and technologies to strengthen its product and R&D pipeline, with a mission to develop groundbreaking therapeutics that address unmet clinical and commercial needs. In 2024,total R&D expenditures was approximately HK$156.6 million, representing 9.4% of the turnover, of which approximately HK$131.6 million were capitalised.

During the year, the Group obtained an approval from NMPA for the registration and commercialisation of the preservative-free unit-dose Diquafosol Sodium Eye Drops and Sodium Hyaluronate Eye Drops (0.3%) in the PRC. The new additions will further enrich its ophthalmic product portfolio and would strengthen its ophthalmology segment of market positioning. In addition, the Group has secured an exclusive agency right in the PRC for SCALGENTM double-layered artificial dermis.

The global phase 3 clinical project of bevacizumab ophthalmic injection (EB12-20145P) has successfully enrolled patients in the PRC, Australia, European Union countries and the United States; the last patient last visit was completed.

The Group holds a total of 100 patents certificates or authorisation letters, comprising 70 invention patents (發明專利), 15 utility model patents (實用新型專利) and 15 design patents (外觀專利).

The Group currently has multiple R&D sites located in Zhuhai (PRC), Boston (USA), London (UK) and Singapore. These sites support our efforts to develop new therapeutics and recruit global talent.

To date, the Group has 16 R&D programmes ranging from pre-clinical to clinical stages, with 4 ophthalmology programs currently in the clinical stage, specifically SkQ1 eye drops, Azithromycin eye drops, Bevacizumab intravitreal injection, and Cyclosporine eye drops, which are aimed at being mid-term growth drivers

Market Expansion and Operational Enhancements

As at 31 December 2024, the Group maintains an extensive network of 44 regional sales offices in the PRC. With a vast distribution network, the Group’s products are prescribed in more than 14,000 hospitals and medical providers, coupled with approximately 1,810 pharmaceutical stores, covering major cities throughout the PRC. The Group’s Singapore base has been gaining good development traction since 2020.

To drive sustainable growth and expansion for its current and future products, the Group has been investing relentlessly in enhancing its competitiveness and broadening its reach by expanding the clinical indications for its commercialised products, targeting lower-tier Chinese cities, fostering complementary sales channels, and leveraging healthtech e-platform to strengthen engagement with patients.

During the year under review, the Group’s near-term production capacity expanded well, driven by

- China Excellent IR - The Best Capital Market Communication Award and The Best Digitalised Investor Relations Award

- Zhuhai Essex Bio-Pharmaceutical Company Limited was awarded as one of the 第六批國家級專精特新“小巨人”企業名單 (The 6th National-Level "Little Giant" Specialised and Innovative Enterprises List).

- Zhuhai Essex Bio-Pharmaceutical Company Limited was awarded as one of the 2023年度TOP100中國化藥企業 (2023 Top 100 Chemical Pharmaceutical Companies in the PRC)

- Beifushu® Eye Drops - 2024 Excellent Brand of Biochemical and Biological Pharmaceutical

- Beifushu® - Chinese reputable medicine brands (in six consecutive years)

Essex Bio-Technology Limited (“Essex” and its subsidiary the “Group”, Stock Code: 1061.HK), a leading biologic Group that develops, manufactures and commercialises genetically engineered therapeutic recombinant bovine basic fibroblast growth factor (“rb-bFGF”). Today, the Group announces its robust annual results for the year ended 31 December 2024.

Despite challenges in the pharmaceutical landscape, Essex Bio-Technology achieved remarkable profitability growth, expanded its market presence, and drove R&D innovation. In the PRC, the pharmaceutical industry faced significant headwinds in 2024, including centralised procurement policies that pressured drug prices and reshaped the competitive landscape.

However, Essex Bio-Technology demonstrated its resilience by adapting swiftly to the evolving market environment, enhancing cost control while ensuring quality assurance, and leveraging its strengths in innovation and operational efficiency. These strategic efforts enabled the Group to deliver steady financial performance and achieve sustainable growth in a challenging year.

Core Products Drive Revenue Growth

The Group delivered net profit growth of 11.6% year-on-year to HK$307.2 million, with the net profit margin improved to 18.4% from 15.8% in 2023. Total turnover for 2024 was approximately HK$1,669.8 million, a 3.9% decrease as compared to HK$1,737.0 million in 2023, primarily due to pricing pressure from the centralised procurement policies in the PRC (“Policy’s Impact”). Despite this, the Group upholds its market position through the broadening of indications for its flagship biologics and expansion of patient access.

The Beifushu® series and Beifuji® series, the Group’s flagship products, continued to be the primary growth drivers, contributing 84.5% of total turnover. The ophthalmology segment recorded a turnover of HK$771.5 million, up 2.2% year-on-year, supported by strong demand for eye care products. The surgical segment generated HK$879.9 million, a decrease of 9.3% due to the Policy’s Impact, but remains a key pillar of the business.

Ample Liquidity and Healthy Financial Position

The Group maintains a healthy financial position, as at 31 December 2024, the Group recorded cash and cash equivalents of approximately HK$557.2 million. Bank borrowings stood at HK$165.3 million, with a distributed repayment schedule: 42.2% repayable within 1 year, 25.5% in 1 to 2 years, and 32.3% in 2 to 5 years. The Group’s gearing ratio improved to 28.8% (2023: 32.0%), reflecting its prudent financial management and strong liquidity.

The Board is pleased to propose a final dividend of HK$6.0 cents per ordinary share. Together with the interim dividend of HK$6.0 cents per ordinary share, the total dividend for 2024 reaches HK$12.0 cents, representing a notable year-on-year increase of 33.3% from HK$9.0 cents in 2023, which demonstrated the Group continues its effort to deliver higher rewards to its shareholders.

Extensive Range of Products Driving Growth in Ophthalmology and Surgical Fields

The Group’s business is primarily made up of the ophthalmology segment (“Ophthalmology”), surgical (wound care and healing) segment (“Surgical”) and provision of services segment. Additionally, the Group is pursuing new therapeutics in oncology, orthopaedics and neurology through strategic investments.

Currently the Group has six commercialised biologics, collectively referred to as the “bFGF Series”, which are marketed and sold in the PRC. Three of the bFGF Series were approved by NMPA as Category I drugs, and four are listed on the National Drug List for Basic Medical Insurance, Work-Related Injury Insurance and Maternity Insurance in the PRC.

In addition to the bFGF Series, the Group has a portfolio of commercialised preservative-free unit-dose eye drops, including Tobramycin, Levofloxacin, Sodium Hyaluronate (0.1%, 0.3%), Diquafosol Sodium and Moxifloxacin Hydrochloride Eye Drops.

Strategic R&D Investment Driving Growth

The Group is committed to pragmatically investing in new products and technologies to strengthen its product and R&D pipeline, with a mission to develop groundbreaking therapeutics that address unmet clinical and commercial needs. In 2024,total R&D expenditures was approximately HK$156.6 million, representing 9.4% of the turnover, of which approximately HK$131.6 million were capitalised.

During the year, the Group obtained an approval from NMPA for the registration and commercialisation of the preservative-free unit-dose Diquafosol Sodium Eye Drops and Sodium Hyaluronate Eye Drops (0.3%) in the PRC. The new additions will further enrich its ophthalmic product portfolio and would strengthen its ophthalmology segment of market positioning. In addition, the Group has secured an exclusive agency right in the PRC for SCALGENTM double-layered artificial dermis.

The global phase 3 clinical project of bevacizumab ophthalmic injection (EB12-20145P) has successfully enrolled patients in the PRC, Australia, European Union countries and the United States; the last patient last visit was completed.

The Group holds a total of 100 patents certificates or authorisation letters, comprising 70 invention patents (發明專利), 15 utility model patents (實用新型專利) and 15 design patents (外觀專利).

The Group currently has multiple R&D sites located in Zhuhai (PRC), Boston (USA), London (UK) and Singapore. These sites support our efforts to develop new therapeutics and recruit global talent.

To date, the Group has 16 R&D programmes ranging from pre-clinical to clinical stages, with 4 ophthalmology programs currently in the clinical stage, specifically SkQ1 eye drops, Azithromycin eye drops, Bevacizumab intravitreal injection, and Cyclosporine eye drops, which are aimed at being mid-term growth drivers

Market Expansion and Operational Enhancements

As at 31 December 2024, the Group maintains an extensive network of 44 regional sales offices in the PRC. With a vast distribution network, the Group’s products are prescribed in more than 14,000 hospitals and medical providers, coupled with approximately 1,810 pharmaceutical stores, covering major cities throughout the PRC. The Group’s Singapore base has been gaining good development traction since 2020.

To drive sustainable growth and expansion for its current and future products, the Group has been investing relentlessly in enhancing its competitiveness and broadening its reach by expanding the clinical indications for its commercialised products, targeting lower-tier Chinese cities, fostering complementary sales channels, and leveraging healthtech e-platform to strengthen engagement with patients.

During the year under review, the Group’s near-term production capacity expanded well, driven by

- A new Blow-Fill-Seal (“BFS”) manufacturing line for Beifushu® unit-dose eye drops installed.

- A new eye gel manufacturing line has been substantially completed, with key equipment installed and production slated to commence in 2025.

Following the appointment of a new general contractor, the Group’s investment in a second factory in Zhuhai, which will have a gross floor area of about 58,000 square metres, has resumed construction in early 2025, with expected completion in 2026-2027 period.

Mr. Patrick Ngiam, Chairman of Essex, commented, “Our ability to deliver robust performances amidst a challenging landscape underscores our unwavering dedication to innovation, operational excellence, and strategic agility. We remain steadfast in our mission to address unmet medical needs, while delivering value to our shareholders. With ongoing R&D investments and market expansion, we are confident in driving sustainable growth and continue making a meaningful impact to the lives of patients”.

~ End ~

About Essex (1061.HK)

Essex Bio-Technology is a bio-pharmaceutical company that develops, manufactures and commercialises genetically engineered therapeutic b-bFGF, with six commercialised biologics currently marketed in China. Additionally, the Company has a diverse portfolio of commercialised preservative-free unit-dose eye drops, Shilishun(適麗順®)(Iodized Lecithin Capsules) and others, which are principally prescribed for wounds healing and diseases in Ophthalmology and Dermatology.

These products are marketed and sold through approximately 14,000 hospitals, supported by the Company’s 44 regional offices in China. Leveraging its in-house R&D platform in growth factor and antibody technology, Essex Bio-Technology maintains a robust pipeline of projects in various clinical stages, covering a wide range of fields and indications.

Website: http://www.essexbio.com

Related news

Multi-Dose Diquafosol Sodium Eye Drops Obtained Approval from NMPA for Commercialisation in China

Multi-Dose Diquafosol Sodium Eye Drops Obtained Approval from NMPA for Commercialisation in China

2025-07-24

Essex Bio-Technology Posts Sound 2023 Annual Financial Results: Revenue Up 29.5%, Profit Up 22.1%

Essex Bio-Technology Posts Sound 2023 Annual Financial Results: Revenue Up 29.5%, Profit Up 22.1%

2024-03-18

Essex Bio-Technology Posts Sound 2023 Interim Financial Results Revenue Up 37.1%, Profit Up 22%

Essex Bio-Technology Posts Sound 2023 Interim Financial Results Revenue Up 37.1%, Profit Up 22%

2023-08-16

The phase 1/2 clinical trial of Bevacizumab for treatment of Ophthalmic Diseases completed

The phase 1/2 clinical trial of Bevacizumab for treatment of Ophthalmic Diseases completed

2023-07-26

Essex Bio-Technology Announces 2022 Annual Financial Results, Resilience & Relevance, Growth Ready

Essex Bio-Technology Announces 2022 Annual Financial Results, Resilience & Relevance, Growth Ready

2023-03-08

Essex Bio-Technology to Present at the 5th China Bio-Pharm Partnering Forum (Bio-Pharm 2021)

Essex Bio-Technology to Present at the 5th China Bio-Pharm Partnering Forum (Bio-Pharm 2021)

2021-10-27

Application for Clinical Trial of Bevacizumab Has Been Approved for the Treatment of wAMD in Latvia

Application for Clinical Trial of Bevacizumab Has Been Approved for the Treatment of wAMD in Latvia

2021-04-20

Essex-Biotechnology Announces Bevacizumab for wAMD Has Received Clinical Trial Approval in Australia

Essex-Biotechnology Announces Bevacizumab for wAMD Has Received Clinical Trial Approval in Australia

2021-01-29

Essex Bio-Technology and Antikor Biopharma Forge Strategic Alliance in FDC for Cancer Treatment

Essex Bio-Technology and Antikor Biopharma Forge Strategic Alliance in FDC for Cancer Treatment

2019-08-02

粤公网安备 44049102496184号

粤公网安备 44049102496184号